When it comes to personal finance, understanding the mechanics behind loans and interest rates can save you from unexpected costs in the long run. One key concept to grasp is the compound interest formula. Whether you’re considering a personal loan for education or any other purpose, having a firm grasp of how compound interest works will empower you to make informed financial decisions.

What is Compound Interest?

Compound interest refers to the interest on a loan or deposit that is calculated based on both the initial principal and the compound interest formula from previous periods. Unlike simple interest, which is calculated only on the principal amount, compound interest grows exponentially over time. This growth can work to your advantage in savings or to your disadvantage when borrowing.

The Compound Interest Formula

The formula to calculate compound interest is:

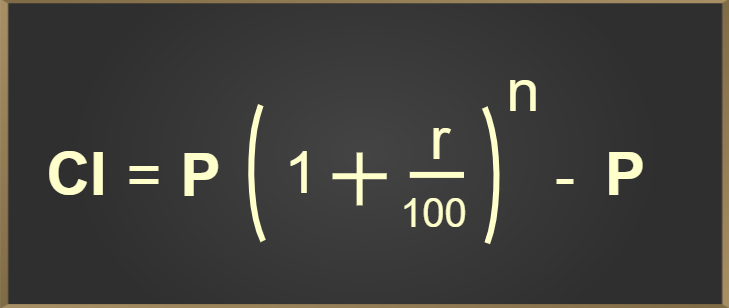

[ A = P(1 + r/n)^{nt} ]

Where:

- A = the future value of the investment/loan, including interest

- P = the principal investment amount (the initial deposit or loan amount)

- r = annual interest rate (decimal)

- n = number of times that interest is compounded per year

- t = the number of years the money is invested or borrowed for

Breaking Down the Formula

To better understand how you can apply this formula, let’s break it down into its components:

- Principal Amount (P): This is the initial amount you are either investing or borrowing. For most personal loans, this amount will be the loan you apply for.

- Annual Interest Rate (r): This is the interest rate charged by the lender. It’s crucial to convert this percentage into decimal form when applying the formula. For example, if the interest rate is 5%, ‘r’ would be 0.05.

- Compounding Period (n): This refers to how frequently the interest is calculated and added to the principal balance. Common compounding intervals include annually, semi-annually, quarterly, monthly, and daily.

- Time (t): Time is measured in years, and it represents the duration for which the money is borrowed or invested.

The Impact of Compound Interest on Personal Loans

When applying for a personal loan for education, understanding compound interest becomes crucial. Loans are generally paid back over time with interest. The longer you take to repay the loan, especially with the compounding effect, the more you will end up paying in total.

Example Calculation

Let’s say you take a personal loan of $10,000 at an annual interest rate of 5% for a term of 5 years. Assuming the interest compounds annually, we can plug the numbers into the formula:

- Principal (P) = $10,000

- Annual Rate (r) = 0.05

- Times Compounded (n) = 1 (annually)

- Time (t) = 5

Using the formula:

[ A = 10000(1 + 0.05/1)^{1 \times 5} ]

[ A = 10000(1 + 0.05)^{5} ]

[ A = 10000(1.27628) ]

[ A = $12,762.81 ]

This means, by the end of 5 years, you would owe approximately $12,762.81, which is a total of $2,762.81 more than what you borrowed. This example illustrates how the compounding effect can significantly increase your total repayment amount.

Factors to Consider Before Taking a Personal Loan

Loan Purpose

Before applying for any personal loan, it’s important to clarify your purpose. If you’re taking a personal loan for education, consider whether the investment will lead to a higher earning potential in the future. Research the return on investment for your chosen field of study and compare this against the interest you’ll incur on the loan.

Interest Rates Comparison

Different lenders offer varying interest rates based on your credit score, loan amount, and repayment term. Therefore, it’s crucial to shop around and compare rates. Even a small percentage difference can significantly affect the amount you pay back over time.

Loan Term

The length of your loan term determines how long you’ll be repaying the loan. While longer terms may lower your monthly payments, they also mean you will pay more in total interest over the life of the loan. Therefore, striking a balance between payment comfort and total cost is essential.

Prepayment Options

Before committing to a personal loan, check if the lender offers prepayment options without penalties. If your financial situation improves, having the flexibility to pay off your loan early can save you money in interest payments.

How to Use the Compound Interest Formula to Your Advantage

- Calculate the Cost of Your Loan: Use the compound interest formula to analyze different loan offers to see how much each one would cost you over time.

- Create a Budget: Understanding compound interest can help you budget more effectively by considering how much you’ll owe after the interest is applied.

- Plan for Early Repayment: If possible, work on a strategy to pay off your loan early, which will save you interest. Using the formula, calculate how much you’ll save if you pay off a portion or the full balance early.

Conclusion

Understanding the compound interest formula is essential for anyone considering a personal loan for education or any other purpose. By grasping how interest accrues over time, you can make informed decisions that help you minimize your financial burden. Remember to consider the total cost of borrowing, shop around for the best interest rates, and plan your repayment strategy carefully. Financial literacy is a powerful tool that can lead to more secure and fulfilling financial futures.